Culture

Celsius is an even bigger dumpster fire than we thought

CEO Alex Mashinsky took over the embattled crypto exchange's trading strategy in January, and proceeded to make some questionable decisions at its helm.

As if Chapter 11 bankruptcy and an ongoing transaction freeze weren’t enough to ruin the credibility of Celsius Network, a crypto lending platform, a Financial Times report published this week exposes just how far mismanagement stretched throughout the company, stemming from CEO Alex Mashinsky at the top.

The CEO reportedly took over the Celsius’s trading strategy back in January ahead of a meeting with the U.S. Federal Reserve because of the possibility of a widespread market crash as Bitcoin and Ethereum prices plummeted.

Reckless abandon — The biggest takeaways from the Financial Times report relates to Mashinsky’s conviction that only he was capable of saving his company, noting that he “personally directed individual trades and overruled executives with decades of finance experience.”

A particularly glaring offense involved the sale of user funds in a deal worth up to “hundreds of millions of dollars’ worth of Bitcoin” before reneging on the decision and buying back the funds a day later — at a loss, of course.

Ultimately, his behavior — especially when taken into account that Mashinsky was dealing with investor funds — highlights the unregulated nature and nascency of the crypto space in general. As noted by the Financial Times, chief executives of large financial institutions rarely involve themselves in trading decisions.

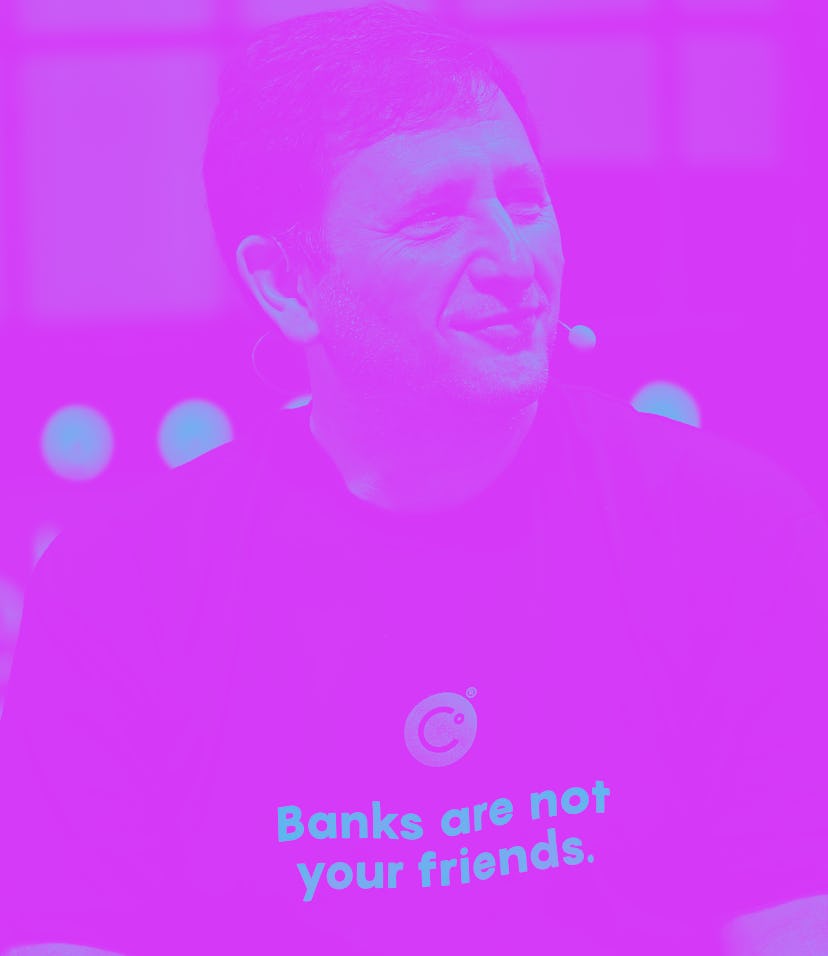

Mashinsky’s decisions only add salt to the wounds, especially when coupled with the way he publicly carried himself in the months leading up to this year’s crypto winter. He would often cite the untrustworthiness of banks, showing up to panels in shirts that read “Banks are not your friends,” or “Party like a crypto whale.”

Mashinky often paraded around the virtues of his business, taking to Reddit and and Twitter, to claim that “[Customer] money is safer in [Celsius] than in a bank,” as outlined in an LA Times column focusing on the fallout of Celsius.

Now, as the company stares a $1.2 billion hole in its balance sheet, and with hundreds of letters written by individual, small-time investors to the judge overseeing the bankruptcy case, the veil over Mashinsky’s leadership is being lifted, and the picture is even worse than it looked from the outside.

While gross mismanagement is bad, only executives who have blatantly engaged in illegal activity like insider trading have received some sort of legal repercussion, so it’s unclear what, if anything, will change as a result of Celsius documented downfall.